Bond Calculations

In this module, you may enter the known variables of the bonds and ask for the unknown one. The varaibles are PV (Present Value which is the fair price), C (Coupon rate in %), r (discount rate or rate of return), Term to maturity (the years till maturity), m (periodicity or number of payments per year). An R script finds the unknown variable for you.

More about the theory and formula

.

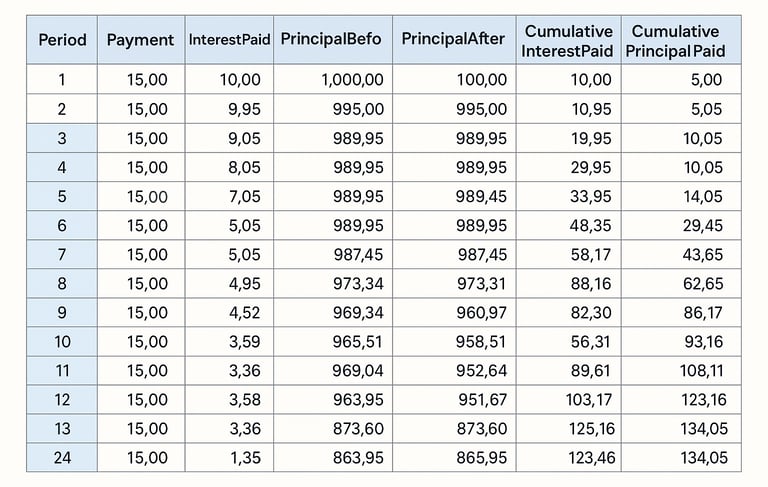

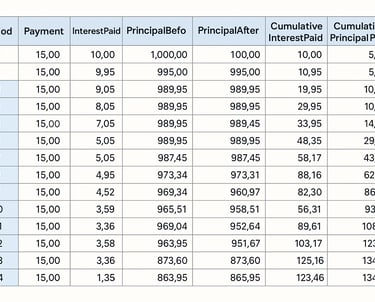

Bond Schedule

In this module, you provide bond informtion and the bond schedule of payment including the interest payment, principal payment, outstanding principal, cumulative interest and cumulative principal are calculated which you can download as an excel file.

More about the theory and formula

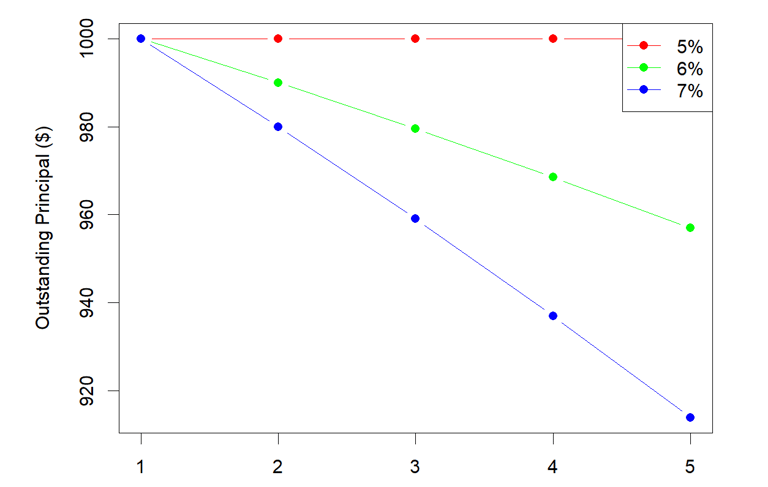

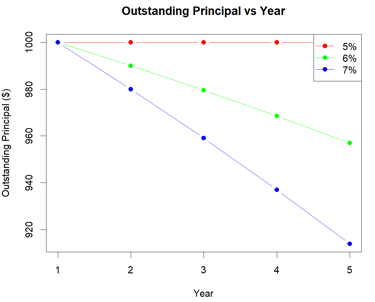

Interest and Principal graph

You enter the bond infomation and get the outstanding principal and cumulative interest paid vs time. By deafalt, the axis are adjsuted for each plot. However, you may keep it unchanged from the previous plot to compare the effect of parameters. Par is 1000 for all plots

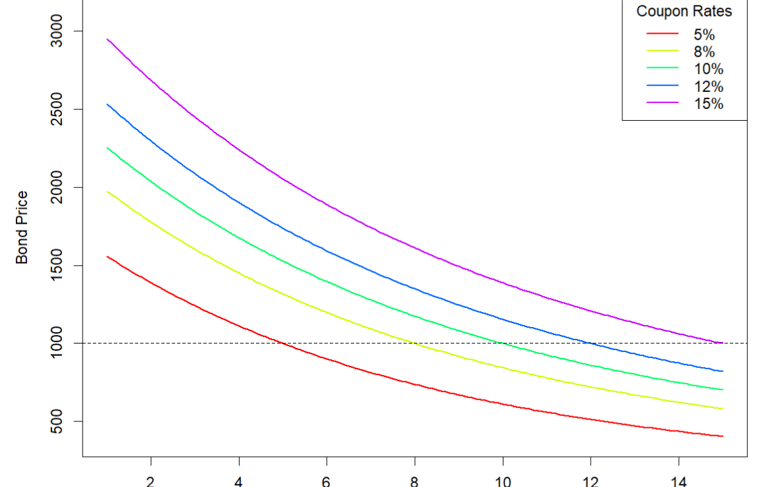

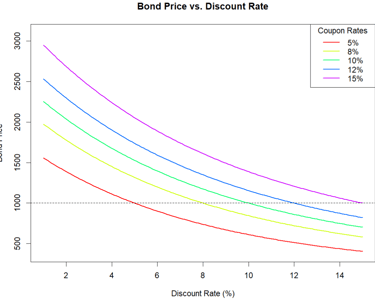

Bond Price vs Discount rate

You enter the bond infomation and get the price vs discount rate plot. You can see convexity effect. Then you may evaluate coupon effect, maturity effect and periodicity effect on the price vs rate curves.

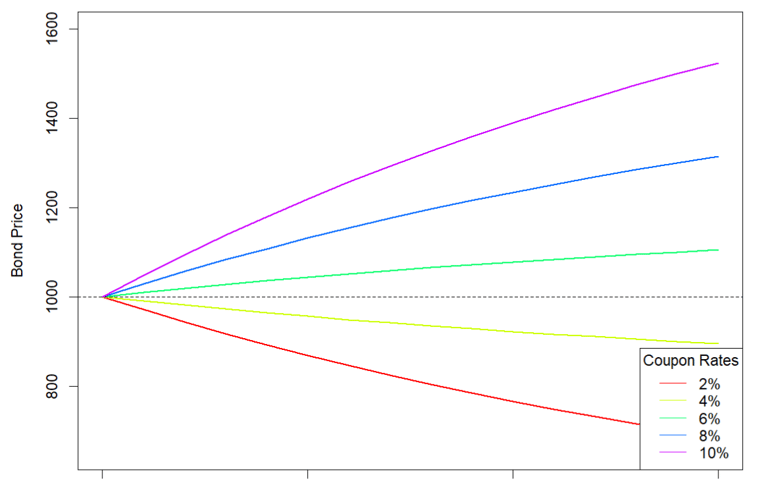

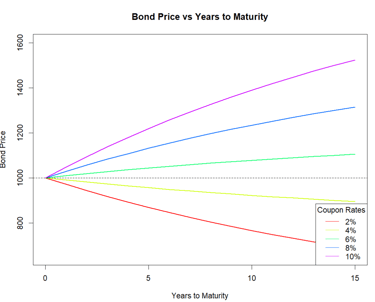

Bond Price vs year to Maturity

You enter the bond infomation and get the price vs year plot. You can You may evaluate coupon effect, maturity effect and periodicity effect on the price vs year to maturity curves.

Bond Price on a specific date

You enter the bond infomation and get the price on a specific date (settlement date) which is between two payments from comounded and linear methods.